As January 2026 approaches, the phrase “federal $2,000 deposit” has begun circulating widely across social media, messaging apps, and online forums. Headlines often assert that payments are already “approved” and will hit bank accounts imminently. For households grappling with high rent, rising grocery costs, and ongoing medical expenses, the idea of an unexpected federal deposit naturally resonates, offering a sense of financial reassurance.

Yet behind the viral claims lies a significant gap between online narratives and official policy. No federal agency has announced a universal $2,000 payment for January 2026. No legislation authorizing such a deposit has been passed, and no official guidance has been issued. Understanding the origins of this story is essential—not only for accuracy, but for protecting personal finances from misinformation and scams.

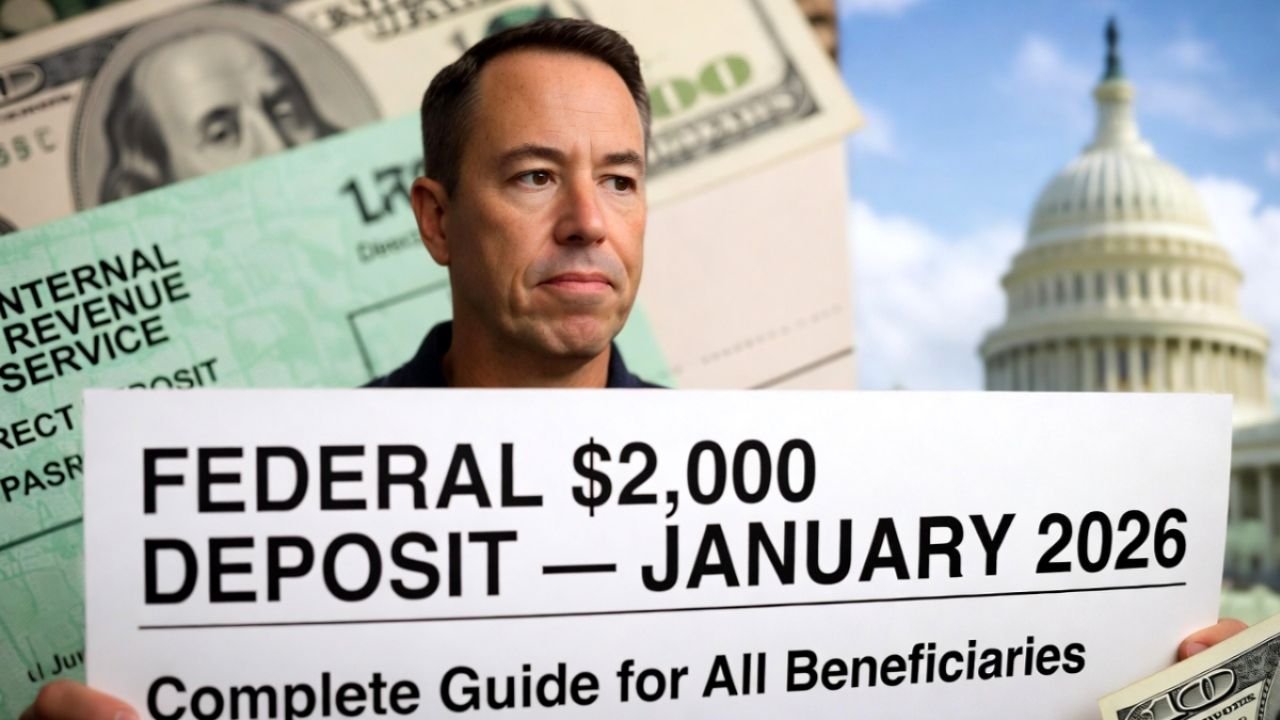

How the $2,000 January 2026 Story Emerged

The current buzz traces back to pandemic-era Economic Impact Payments, when large deposits arrived automatically for millions of Americans. Amounts like $1,200, $1,400, or $2,000 became psychologically associated with government relief, and that expectation lingers.

Since then, discussions about tax rebates, deficit offsets, and targeted relief have circulated in policy circles. Many of these proposals never reach implementation. On social media, nuanced policy debates are often condensed into definitive claims of “approved” payments. By the time these messages spread, the distinction between proposal and policy disappears.

What Federal Agencies Have Actually Said

Official communication from the IRS, U.S. Treasury Department, and Social Security Administration remains consistent: there is no nationwide $2,000 direct deposit scheduled for January 2026. No legislation authorizing such a payment exists, no budget allocations have been made, and no formal rollout guidance has been released.

Historically, federal payments of this scale follow a visible public process. Legislation moves through Congress, media reports track progress, and agencies issue coordinated statements before any funds are disbursed. A payment of this size does not happen quietly.

Why Some Americans May Still See Deposits Around $2,000

Timing plays a major role in the confusion. Early 2026 coincides with the start of tax refund season, when many households receive refunds in the $1,500–$2,500 range due to refundable credits like the Earned Income Tax Credit or Child Tax Credit. When these funds are deposited under “US Treasury,” they can easily be mistaken for stimulus-style payments.

In addition, delayed corrections from prior tax years, amended returns, or benefit reconciliations can trigger lump-sum deposits. Social media amplification of these individual experiences often transforms routine refunds into the perception of a national program.

Targeted Payments and Misinterpretation

Some legitimate, limited federal payments do exist. Veterans, military families, and certain federal employees occasionally receive one-time allowances, back pay, or benefit adjustments. These payments are fully documented but apply only to specific groups.

Online summaries frequently omit eligibility details, creating the impression that the payment is universal. Economist Rahul Mehta explains: “People see a number and assume universality. The eligibility conditions disappear, and the payment takes on a life of its own.”

The Scam Economy Around False Claims

Whenever rumors of federal money circulate, scammers quickly exploit the confusion. Fake emails, text messages, and websites promise to “release” the $2,000 deposit once banking details are provided. Many even copy official IRS logos and language to create urgency.

Consumer protection experts warn that the absence of a real program creates a dangerous information vacuum. Cybersecurity analyst Maria Lopez notes, “When there’s no real programme, there’s nothing to verify against. That makes people more vulnerable to impersonation scams.” The safest approach is simple: never provide personal information in response to unsolicited requests.

Why the Rumor Persists

Economic stress fuels the ongoing narrative. Even as inflation moderates, many households continue to feel financial pressure. The promise of a federal deposit provides emotional comfort, regardless of its basis in fact. Social media dynamics amplify certainty over nuance, rewarding bold claims over careful explanations. Over time, repeated assertions create a sense of legitimacy—even when agencies deny them.

If Real Relief Does Arrive, What Would It Look Like?

Policy analysts agree that any future relief would likely be targeted rather than universal. Lawmakers have repeatedly signaled a preference for tax credits, benefit expansions, or sector-specific assistance instead of blanket payments. Any approved program would be accompanied by formal legislation, public hearings, and detailed guidance on eligibility and distribution timelines.

Staying Informed and Safe

Until official announcements are made, caution is the most important tool. Taxpayers should:

- Verify information through official agency websites (IRS, Treasury, Social Security Administration)

- Understand the difference between tax refunds, benefit adjustments, and relief payments

- Treat viral claims with scepticism to avoid scams and financial missteps

As one consumer advocate notes, “Relief programs don’t rely on rumours to reach people.” In today’s digital environment, verification remains the only reliable safeguard.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Federal payment schedules, programs, and eligibility rules are subject to change. Readers should consult official federal agency sources or qualified professionals for guidance specific to their circumstances.